It happens: The business of governing is hard at the best of times, and these are not the best of times. All governments run out of ideas eventually but this particular incarnation of the Tory party ran out of steam earlier than most. While it can point to mitigating circumstances in the form of the pandemic, it has made a series of unforced errors that have contributed to its unpopularity. Although it made mistakes prior to 2016 (who didn’t?), the Brexit outcome changed the calculus. The government chose to accept a close-run advisory plebiscite as a winner takes all contest with no plan how to deliver. Not only did it waste considerable amounts of political capital trying to reach an accommodation with the EU but it failed to implement any of the changes that were promised by Brexit proponents. Even more egregious was its failure to understand the lessons of the 2019 election. The thumping majority gained by Boris Johnson was not a vote in favour of populist nationalism, as many in the party believed, but the imprimatur of an electorate willing to believe Johnson’s claim that he could finally get Brexit done and – equally importantly – was a repudiation of the policies espoused by Jeremy Corbyn.

There are no guarantees in politics but it is a raging certainty that Labour will win the next election. Latest bookmakers odds put the probability of a Labour win at 89.8% versus 4.3% for the Tories (and a 14.9% likelihood of a hung parliament). Although bookies odds reflect the weight of money being placed rather than an objective assessment (see this post from 2019), the fact that a record number of 83 Conservative MPs have so far opted to stand down, rather than contest their seats in July, is one indication of the party’s pessimism. Electoral Calculus currently estimates that Labour will win 479 seats (see below) which would give it the biggest majority (308) of any government since 1918 (bar the emergency National Government of 1931). For the record, I would be astounded if such a majority is achieved - Labour will do well to emulate Blair's 1997 landslide.

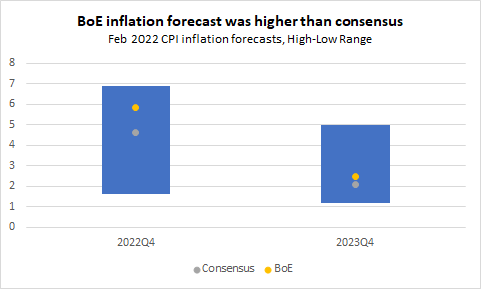

The economy will be one of the key areas where Labour and the Conservatives will lock horns during the campaign. Sunak’s quite literal damp-squib announcement on Wednesday argued that: “Our economy is now growing faster than anyone predicted, outpacing Germany, France and the United States. And this morning it was confirmed that inflation is back to normal. This means that the pressure on prices will ease, and mortgage rates will come down. This is proof that the plan and priorities I set out are working.”

This is not wholly wrong, but not wholly right either. It is true that UK growth outpaced the three other countries in Q1 2024 but since 2016 has outpaced only Germany. In any case, it is not just the rate of growth which matters: IMF data suggest that UK real incomes per head are almost 30% below US levels and 12% below German levels (chart above), with the rankings not having changed much since 2010 (indeed, they have widened relative to the US). One potential cause of the dissatisfaction with government in recent years has been the extent to which voters do not feel better off. It is important to recognise at the outset that this is not simply a problem in the UK: It is an issue across much of the industrialised world, notably Europe. But this cuts no ice with voters who, not unsurprisingly, are focused on their own domestic issues. The Conservative government of 1979 to 1997 delivered real household disposable income growth averaging 2.7% per annum, while the Labour government of 1997 to 2010 presided over annual growth of 2.5%. Since 2010, this has slowed to 1.3% (chart below).

This is a reflection of changed circumstances following the GFC in 2008, with the slowdown in productivity growth at the heart of the problem, slowing to around 0.5% per year versus 1.5% pre-2008. The Productivity Institute has identified three key reasons for the UK’s sluggish performance in this regard: (i) Underinvestment, in both physical and human capital; (ii) Inadequate diffusion of productivity-enhancing practices from the innovation-driven sectors areas to the wider economy and (iii) Institutional fragmentation and lack of joined-up policies, aggravated by the dichotomous arrangement whereby the policy formation process is highly centralised but the institutional framework responsible for translating this to the wider economy is highly fragmented. None of these will be an easy fix, but they will require a root-and-branch reform of the policy formulation process. Market solutions alone will be insufficient to deliver the desired outcomes, and certainly not on a five-year horizon.

The fiscal constraint

One of the key issues that voters care about is the state of the UK health and social care sectors. Public dissatisfaction with the NHS reached an all-time high in the 2023 Social Attitudes Survey, reaching 52% compared to the previous peak of 50% in 1997. Ironically, given the current government’s desire to reduce taxes, almost half of voters support a policy of raising taxes to provide additional NHS funding. With an ageing population placing increased strain on the health services at a time when post-pandemic strains and funding challenges have raised pressure on the system, there may be little option but to test the public’s willingness to pay higher taxes. The alternative may be to explore more radical funding options, such as a continental European-style social funding model; increased hypothecation; raising NHS charges or relying on greater private sector provision.

None of these are likely to be very palatable to the electorate but with the UK’s debt-to-GDP ratio already at its highest in 60 years, at around 100%, and competing demands from defence and managing the green transition, the fiscal constraint is increasingly biting. It is thus clear that the UK will require a serious debate about its policy choices in the next parliament. At the very least a radical reform of the tax system should form part of the political and economic debate with nothing off the table. Even if they are not adopted, it is necessary to have a debate about the pros and cons of wealth taxes and land taxes, if only to widen the nature of the debate.

Final thoughts

In some ways, the 2024 general election will not be a good one to win. Many challenges lie ahead and they will require the next government to make some unpopular choices. Just as 1979 marked a break with the post-1945 political consensus, so it is time to make a break with the post-1979 settlement which has peddled the view that it is possible to reduce the size of the state and reduce taxes while simultaneously driving up living standards. Achieving the latter will require compromises with regard to the former and more radical thinking on a whole range of issues. But as this bitter election campaign gathers momentum, voters will do well to remember that there are no quick fixes to the economic problems facing the UK. Liz Truss reckons there are Ten Years To Save the West, and while I am not in the habit of taking lessons from one who failed to outlast a lettuce, ten years to fix the economy might not be too far wide of the mark.